A concerned citizen raised the issue of possible financial misrepresentation from the Port of Olympia’s during their commission meeting last Mon., Oct. 11.

In the public hearing, Denis Langhans, of Olympia, said that it is deceptive for the Port to consider the operating income before depreciation as cash earned from operations. Langhans said, “That’s either delusional or [a] deceptive statement because that’s not true.” He continued, “what presented to the public as free and clear cash flow is certainly not free and clear. That $2.3 million gets eaten up pretty damn fast by the $4.6 million worth of bond principal and interest that’s paid out.”

Operating income before depreciation

Generally, operating income before depreciation is used to measure whether a business is profitable. It usually excludes expenses on assets such as equipment, or investments that may carry a debt.

In response, Commission Chair Joe Downing argued that the line item refers to the income before the depreciation, and not after. He claimed, “Just in terms of your main statement that operating income before depreciation means cash earned from operations. Well to me you’re reading something into that because the proper accounting line item is operating income before depreciation.”

Downing also said that he had tried to compare the Port of Olympia’s financial budget with other ports in the region. “I did take a look at other ports. Tax revenues and bond payments are all part of the non-operating income.” Downing said that another port district had reported their “net income after depreciation is negative $1 million.” He refused to name that other port, and added that another port also published a “net operating income just barely positive of $45,000 from $15 million revenue after depreciation.”

The commission chair also assured that the current outcome had taught them to be more cautious. “I hope we’re super careful with future investments,” Downing said.

Misrepresentation

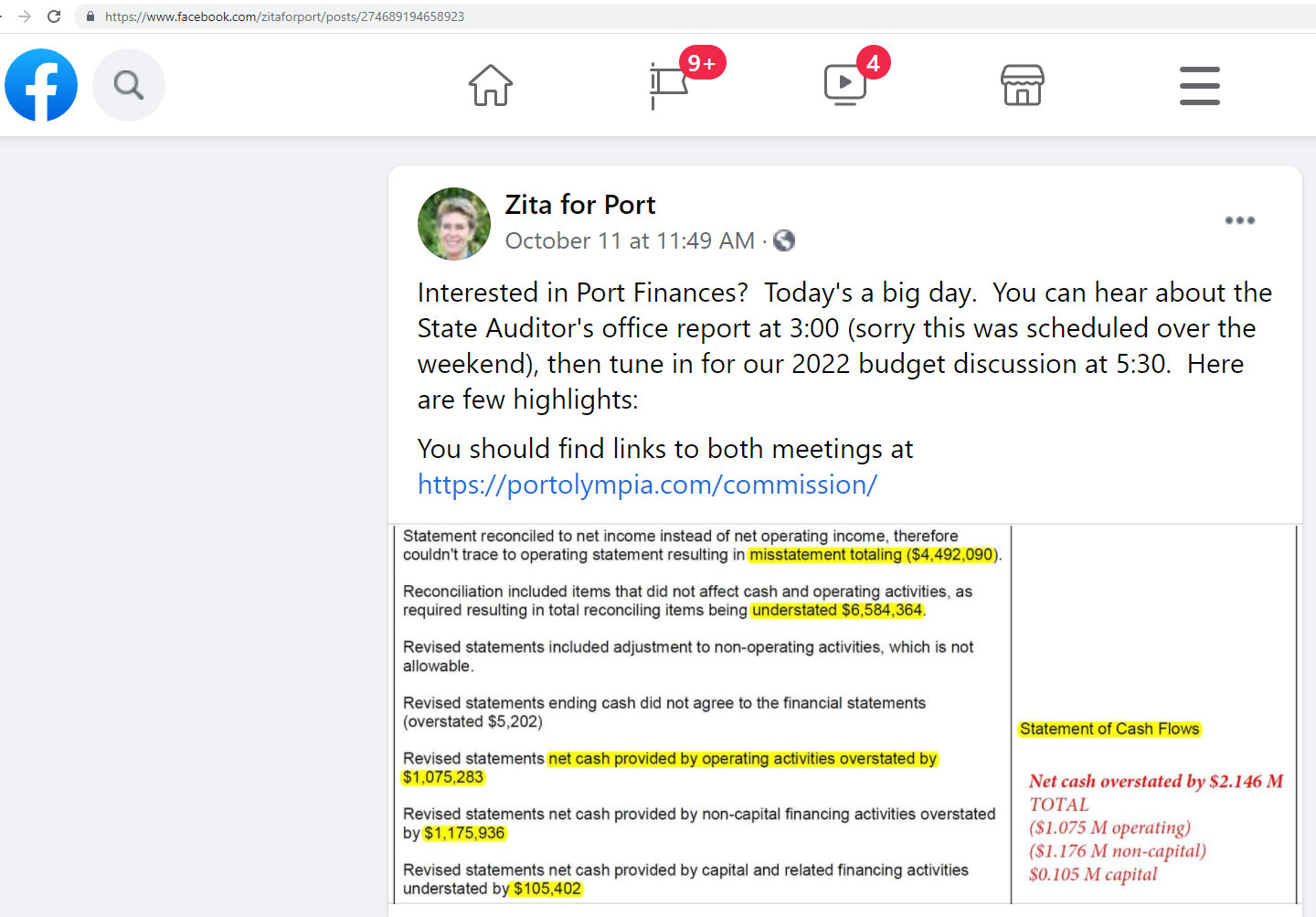

Commissioner E.J. Zita responded to Langhans’ concern by adding that the Port had also misrepresented several line items in their financial report. Zita shared that according to the State Auditor Office (SAO), “Our cash flow is one of several things that have been reported inaccurately by $2.26 million.”

She continued, “There are two other categories that have been misreported by four and a half million dollars in one case and six and a half million dollars in another case.” She believed that there are some serious concerns about the Port’s cash flow. “Do we have enough?” and “Are we reporting it accurately?” the commissioner asked.

In addition, Zita had also uploaded parts of the SAO report on a Facebook post. (See image above this story.)

Commissioner Bill McGregor did not comment on the issue of the Port’s financial misrepresentation. Instead, he thanked Langhans for sharing his concerns.

General obligation bonds vs. general revenue bonds

Aside from the discrepancies in the operating income before depreciation, Langhans also shared that there is an issue with the use of general obligation bonds versus the revenue bonds. “It does points out the problem of general obligation bonds. Now, they’re certainly cheaper than going general revenue so I can see that attraction,” Langhans said.

“The problem is, is that the general revenue bond would require a thriftier underwriting but I submit that the problem with the Port, why we are in such a hole, is that there is no underwriting in terms of due diligence. I mean the things that we cover under general obligation bonds, I mean they just don’t fly, they’re not viable. And so, we’re using a device to finance a thing that’s really not fair to the public.”

Revenue bonds are tied to a specific revenue source such as docks, highways, or other capital facilities. On the other hand, a general obligation bond is not backed by a project or a specific revenue source. Rather, these types of bonds are supported by the taxpayers.

Zita also agreed with Langhans’ suggestion to use revenue bonds instead of general obligation bonds. “Your point is well taken that general obligation bonds are cheaper than they can be used to finance projects with little oversight.” She said that the Port has utilized general obligation bonds to purchase equipment such as log loaders, and a crane as well as in financing projects such as the Lacey CBD building, which resulted in the Port losing money. “We didn’t do a market study ahead of time. And we didn’t have to because it is backed by the taxpayers, the rich daddies,” Zita said.

Downing disagreed. He explained that the log loaders are not “hugely” profitable since they charge at an hourly rate. While Downing recognized that there had been previous issues with the Lacey CBD the port staff was able to “get that investment into shape.”

“I can’t speak to whether or not we did right or wrong, in terms of revenue bonds or general bonds,” Downing said.

Comments

No comments on this item Please log in to comment by clicking here